Higher US inflation figures, consumer sentiment drops with a rise in inflation expectations

Previous week’s events (week 08 - 12.04.2024)

Announcements

US economy

The University of Michigan’s preliminary reading on the overall Consumer Sentiment index was reported low, at 77.9 this month, compared to a final reading of 79.4 in March. Inflation expectations for the next 12 months and beyond increased as a survey showed on Friday.

One-year inflation expectations increased to 3.1% in April from 2.9% in March, rising just above the 2.3-3.0% range seen in the two years before the COVID-19 pandemic. The survey’s five-year inflation outlook rose to 3.0% from 2.8% in the prior month.

Inflation

United States

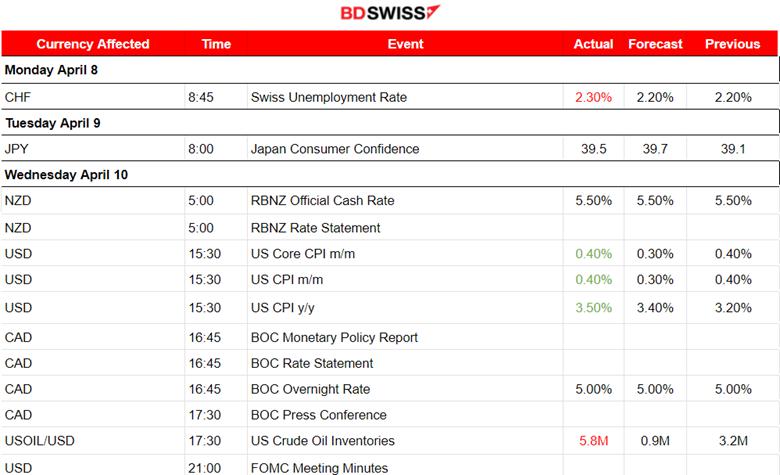

The U.S. inflation report last week shook the markets as it showed that U.S. consumer prices increased more than expected in March leading financial markets to anticipate that the Federal Reserve would delay cutting interest rates until September.

The latest labour market data showed that job growth accelerated in March, with the unemployment rate down to 3.8% from 3.9% in February. Financial markets now expect only two rate cuts instead of the three envisaged by Fed officials last month. A minority of economists see the window for rate cuts closing. The central bank has kept its policy rate in the 5.25%-5.50% range since July. It has raised the benchmark overnight interest rate by 525 basis points since March 2022.

According to the PPI data, U.S. producer prices increased moderately in March calming fears of a resurgence in inflation. Milder increases in the inflation measures are expected after this release. However, the recent CPI inflation report was quite strong.

Interest rates

BoC

The Bank of Canada (BOC) kept its key interest rate unchanged at a near 23-year high of 5% on Wednesday but the bank’s head said a cut in June was possible if a recent cooling trend in inflation is sustained.

Inflation has been falling in recent months but at 2.8%, it is still above the bank’s 2% target.

“We just need to see it for longer to be confident that we are clearly on a path to 2% inflation and when we are at that point it will be appropriate to reduce our interest rate,” Governor Macklem told reporters.

ECB

The European Central Bank (ECB) kept interest rates steady at record highs but gave a clear signal that it may be preparing to proceed with cuts as inflation is heading towards the target level.

The central bank kept its deposit rate at 4.0%, where it has been since September. But, with inflation now close to the ECB’s 2% target, the ECB gave hints about a possible cut at its next meeting.

With Thursday’s decision, the ECB also left the interest rate on its daily and weekly loans for banks at 4.75% and 4.50% respectively.

Currency markets impact – Past releases (week 08 - 12.04.2024)

Server Time / Timezone EEST (UTC+02:00).

- RBNZ held the OCR at 5.50% in hopes of the return of the CPI inflation to the 1% to 3% target in 2024. NZD was affected by an overall appreciation of the currency. NZDUSD moved near 20 pips upwards.

- The U.S. inflation data (CPI) caused a shock as the figures surprised the markets by beating expectations. A higher-than-expected inflation caused a Dollar Index surge challenging expectations of an imminent rate cut. US Consumer Price Index (CPI) figures outpaced forecasts for the fourth consecutive month, reaching 3.5% over the 12 months to March. Now a June rate cut seems less likely after the hot CPI. Gold prices faced downward pressure amidst a strengthening U.S. Dollar.

- The Bank of Canada (BOC) has left the target for the overnight rate at 5%, in line with market expectations, and is continuing with its policy of quantitative tightening. No major impact on the market was recorded at that time.

- China’s Consumer Price Index (CPI) rose 0.1% YoY in March, down from a 0.7% growth in February. The market forecast was for a 0.4% increase. Chinese CPI inflation came in at -1.0% over the month in March versus February’s 1.0% rise. China’s Producer Price Index (PPI) fell 2.8% YoY in March, compared with a 2.7% drop seen previously. No major impact was recorded at that time. USDCNH was following a slight intraday drop during the release.

- The European Central Bank (ECB) decided to hold interest rates steady for a fifth straight meeting and gave a strong signal that cuts are on the way despite the uncertainty in regards to the Fed’s decisions from now on after strong data in regards to the economy’s labour market, business and inflation. At the time of the release, the impact was not great but eventually, the result was EUR depreciation and dollar appreciation bringing the EURUSD down. The dollar index moved to the upside.

- Producer Price Index (PPI) data reports for the U.S. on the 11th of April showed that prices for final demand rose 0.2 percent in March. Final demand prices moved up 0.6% in February and 0.4 % in January. Excluding food and energy, core PPI also rose 0.2%, meeting expectations. The USD strengthened after the release.

- Unemployment claims were reported lower at 211K confirming a stronger labour market and coinciding with the hot NFP report.

- U.K.’s Real gross domestic product (GDP) is estimated to have grown by 0.1% in February 2024, following growth of 0.3% in January 2024 (revised up from 0.2% growth in our previous publication). The U.K. entered a technical recession at the end of 2023 after data showed two quarters of economic contraction. No special impact on the GBP at that time.

- The Prelim UoM Consumer Sentiment report showed that the Consumer Sentiment Index in the U.S. declined 1.9% in April compared to the month prior. The figure surged 22.3% on an annual level. The Index of Consumer Expectations dipped by 0.5% on a monthly basis but grew 27.1% on a yearly basis, coming in at 77. Year-ahead inflation expectations ticked up from 2.9% last month to 3.1% this month. No major impact was reported in the market.

Forex markets monitor

Dollar Index (US_DX)

It was an important week for the dollar and the Federal Reserve (Fed) as the inflation report had a major impact on the market and especially expectations for the future of the USD and inflation. It was on the 10th of April during the inflation report release for the U.S. that the dollar index jumped after the release of higher-than-expected inflation figures that shook the market. The PPI figures were having a similar effect as they were reported in line with expectations. The market reacted with dollar appreciation and a change in expectations of when the interest rate cuts will take place eventually. The market participants now anticipate that the Fed will delay cutting interest rates until September. This fact caused the dollar surge that lasted until even to this day.

EUR/USD

The pair was moving sideways until the inflation report release on the 10th of April when the volatility levels reached extremely high levels. The dollar experienced strong appreciation causing the EURUSD drop of near 130 pips that day. The ECB decided to keep rates steady on the 11th of April and according to their statements cuts should take place soon. This obviously causes the EUR’s weakening. In combination with the USD strengthening, the EURUSD inevitably continued with the downward movement, with the USD however, mostly driving the path.

USD/JPY

Due to the dollar strengthening after the inflation news for the U.S., the USDJPY moved to the upside. The 11th - 12th of April was a period of low volatility and the price was actually moving within a channel but it was having an upward heading. However, the pair was moving around the 30-period MA when eventually on the 15th of April the USDJPY took a rapid move to the upside. Recent information shows that the Bank of Japan is shifting to a more discretionary approach in setting policy, with less emphasis on inflation according to sources, as the central bank maps its monetary path following the historic change in interest rate policy ending eight years of negative rates.

Crypto markets monitor

BTC/USD

Bitcoin is trading below 71K USD which was the peak last week on the 12th of April. Since then the price of bitcoin fell rapidly during the weekend reaching the lowest support near 60,280 USD level before retracing to the 30-period MA. Currently, the price crossed the 30-period MA suggesting the end of the short-term downtrend with hopes that volatility would turn to higher levels and potentially cause the price to reach the 71K USD level again soon.

Next week’s events (week 15 - 19.04.2024)

Coming up

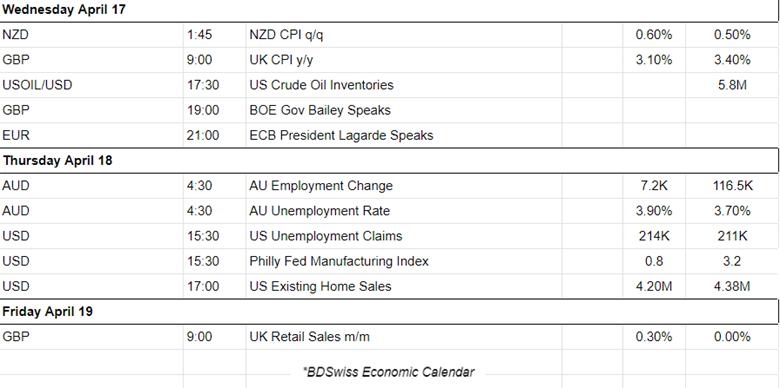

Inflation reports for Canada, New Zealand and the U.K.

Retail Sales Reports for the U.S. the U.K. and China.

We have also the release of important employment data for the U.K. and Australia.

Currency markets impact

- On the 15th April retail sales reports for the U.S. are going to be released at 15:30. These figures will be vital in understanding if eventually, sales will coincide with the strong labour market data and business data. They are expected to see growth again with the core figures expected to show more growth than previously reported. USD pairs could be affected by an intraday moderate shock.

- China retail sales and GDP figures will be released on the 16th during the Asian session. The forecasts are somehow pessimistic about the economy as the figures are expected to be worse than previous. The pairs affected could be the CNH and AUD pairs. No major shocks are expected though in the market.

- At 9:00 the employment data ( Claimant Count change) and labour market report for the U.K. could cause high volatility or even an intraday shock for the GBP pairs during the release.

- At 15:30 the inflation report for Canada could cause intraday shock for the CAD pairs. The monthly figure is actually expected to be reported higher. In the case of a surprise to the upside, the CAD should see significant appreciation.

- On the 17th of April, the inflation data (quarterly)for New Zealand will be reported during the Asian session. A higher figure is expected. If the actual figure is close to the forecast now major impact is expected in the market. Any surprise could cause the NZD pairs to deviate from the intraday mean but retarcements should happen quickly.

- At 9:00 the U.K. Inflation figure release could cause intraday shock and higher volatility levels for the GBP pairs during the release. Inflation is expected to be reported way lower. However, considering the economic conditions lately on a global scale we might not see such a low figure. In that case, the GBP could momentarily appreciate.

- Employment data for Australia will be released on the 18th of April and are expected to affect the AUD pairs greatly. Employment change is expected to be reported way lower and with a higher unemployment rate. The Reserve Bank of Australia increased the Cash Rate to 4.35 on Nov 7, 2023, and remains at that level until today. Inflation remained steady at 3.4% for 3 times in a row so far.

- On the 19th of April, the monthly retail sales report of the U.K. will be released and the figure is expected to be reported higher. The GBP pairs could see higher volatility at the time of the release as there is an absence of other significant news and releases.

Commodities markets monitor

US Crude Oil

Following Iran's weekend attack on Israel, the price actually dropped flirting with the 84.3 USD/b again. That seems a critical support and its breakout could cause a significant drop. On the 12th of April, Crude oil experienced a sudden drop after 18:00 and the start of the N. American session.

The alternative scenario will depend on the main fundamental factors such as Israel's reaction to the attack which will be key to global markets in the days and weeks ahead. Significant and longer-lasting price effects for a price increase instead would require a material disruption to supply.

Gold (XAU/USD)

It has been a long time since Gold has been quite resilient to the downside, even when we have news releases that cause the dollar to strengthen. The NFP data release did not manage to bring it down. The U.S. inflation report caused a heavy dollar strengthening but again Gold was not affected by a heavy drop, but rather kept its resilience. Currently, the U.S. dollar strengthening is in place and metals see more demand kicking in causing prices to rally. However on the 12th of April, Gold experienced a sudden drop after 18:00 and the start of the N.American session just like the price of oil. It seems that positions on these commodities have been closed ahead of the weekend, perhaps due to increased uncertainty.

Equity markets monitor

S&P500 (SPX500)

Price movement

A higher-than-expected inflation figure for the U.S. was released. This means that borrowing costs will remain high for a long time, causing a drop in U.S. indices on the 10th of April. The index found support near the 5,135 USD level before retracement took place. On the 11th of April, the index eventually saw a sharp movement upwards reaching the resistance at near 5,215 USD without retracement taking place. On the 12th of April, volatility continued being high and the index suffered a huge drop breaking the support at 5,135 USD, reaching the next level at 5,100 USD before eventually retracing to the 30-period MA. The RSI shows currently bullish signals even though it is not so clear.

Reprinted from FXStreet,the copyright all reserved by the original author.

Disclaimer: The content above represents only the views of the author or guest. It does not represent any views or positions of FOLLOWME and does not mean that FOLLOWME agrees with its statement or description, nor does it constitute any investment advice. For all actions taken by visitors based on information provided by the FOLLOWME community, the community does not assume any form of liability unless otherwise expressly promised in writing.

FOLLOWME Trading Community Website: https://www.followme.com

Hot

No comment on record. Start new comment.